Singapore’s private residential property market showed further signs of cooling in the second quarter of 2025, with the Urban Redevelopment Authority’s (URA) flash estimates indicating a 0.5% quarter-on-quarter (q-o-q) increase in the overall private residential property price index. This marks the second consecutive quarter of slowing growth, following a 0.8% increase in 1Q 2025 and a robust 2.3% rise in Q4 2024.

More striking, however, is the sharp 40% drop in transaction volume, with only 4,340 units sold in 2Q, down from 7,261 units in 1Q. On a year-on-year basis, sales activity declined approximately 12%, underscoring the effects of fewer new project launches and a more cautious stance among homebuyers amid a shifting economic backdrop.

Segmental Performance Snapshot

The moderation in price growth was observed across both landed and non-landed segments, though regional disparities in performance were stark:

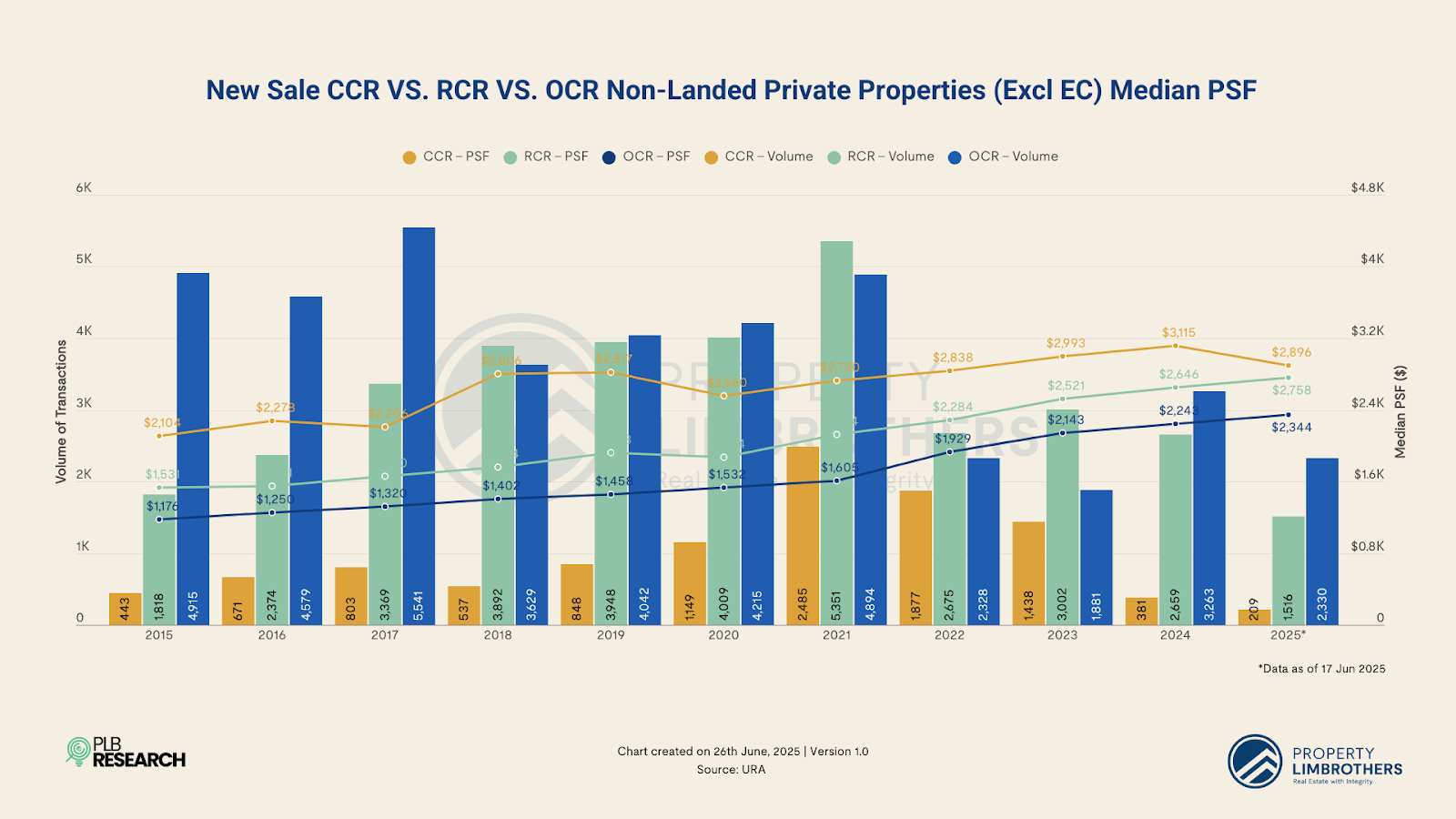

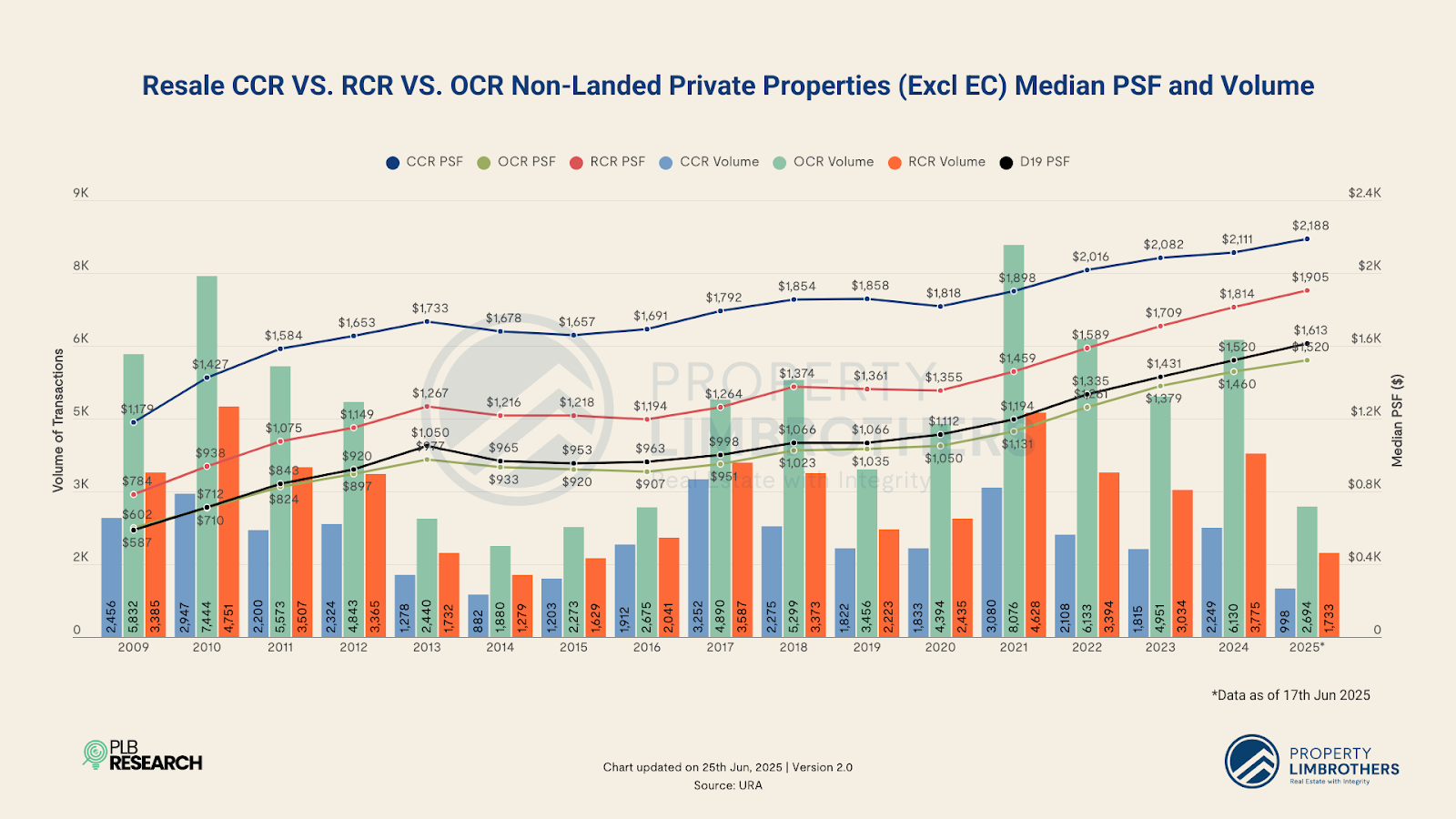

CCR rebounded sharply in Q2, posting a +2.3% increase after a q-o-q decline in 1Q. This turnaround was largely driven by new launches at benchmark prices, such as that of One Marina Garden, which lifted average transacted prices.

RCR saw a price correction of −1.1%, following outsized gains in 1Q.

OCR continued its steady climb with a +0.9% rise, highlighting consistent demand from upgraders and value-conscious buyers.

Singapore’s private property market is increasingly entering a consolidation phase, shaped by three converging dynamics:

The 2Q 2025 data affirms that Singapore’s private residential market is transitioning into a consolidation phase. After nearly two years of strong price appreciation, the market is now contending with a mix of demand-side fatigue, strong pipeline of upcoming supply, and growing macroeconomic headwinds.

The moderation in price growth to just 0.5%, coupled with a substantial 40% plunge in transaction volume, reflects waning urgency among buyers.

A key development this quarter is the divergence in regional performance. The CCR has emerged as the relative outperformer, supported by resilient demand for premium homes, a narrowing price gap with RCR and OCR properties (as seen from figures above), and investor confidence in long-term asset value retention in prime districts.

In contrast, the RCR has begun to show signs of weakness, with prices declining 1.1%—a signal that the market may be recalibrating expectations after rounds of increase in earlier quarters. The OCR remains relatively stable, driven by HDB upgraders’ demand and better affordability.

At the macro level, the broader economic environment is casting a shadow over property sentiment. The Singapore government has flagged moderating GDP growth, tightening global trade conditions, and early signs of softening labour demand as key risks heading into the second half of 2025.

With these uncertainties, both buyers and financial institutions are likely to adopt a more cautious approach, especially in terms of mortgage financing and risk assessment. The government’s ongoing strategy to ensure ample supply—with nearly 10,000 private residential units planned under the Government Land Sales (GLS) programme in 2025, a 50% increase from the 2021–2023 average—is expected to further anchor price expectations and reduce speculation-driven pressure.

Taken together, these factors point toward a more balanced market in the quarters ahead.